Table of Contents

Investing Costs

For those who save for retirement, the greatest asset allocation is that which offers the maximum returns, with an acceptable level of threat. Having said that, possibility-altered returns will not right deal with the requirements of people who are retired, for the reason that they have a tendency to take in alternatively than accumulate. What matters most for all those who have ceased working is not portfolio advancement, but as an alternative expending energy.

Consequently, the top quality of a retiree’s allocation is usually evaluated by the withdrawal level that it permits. What share of assets can the retiree safely devote? The response to that query contains many transferring elements, together with: 1) the retiree’s life span, 2) the variability of spending, and 3) the price of investment return. Typically, the issue is simplified by repairing the to start with two inputs. The daily life span is set at 30 years, and the paying strategy is static, with each individual year’s withdrawal matching the past year’s volume, immediately after changing for inflation.

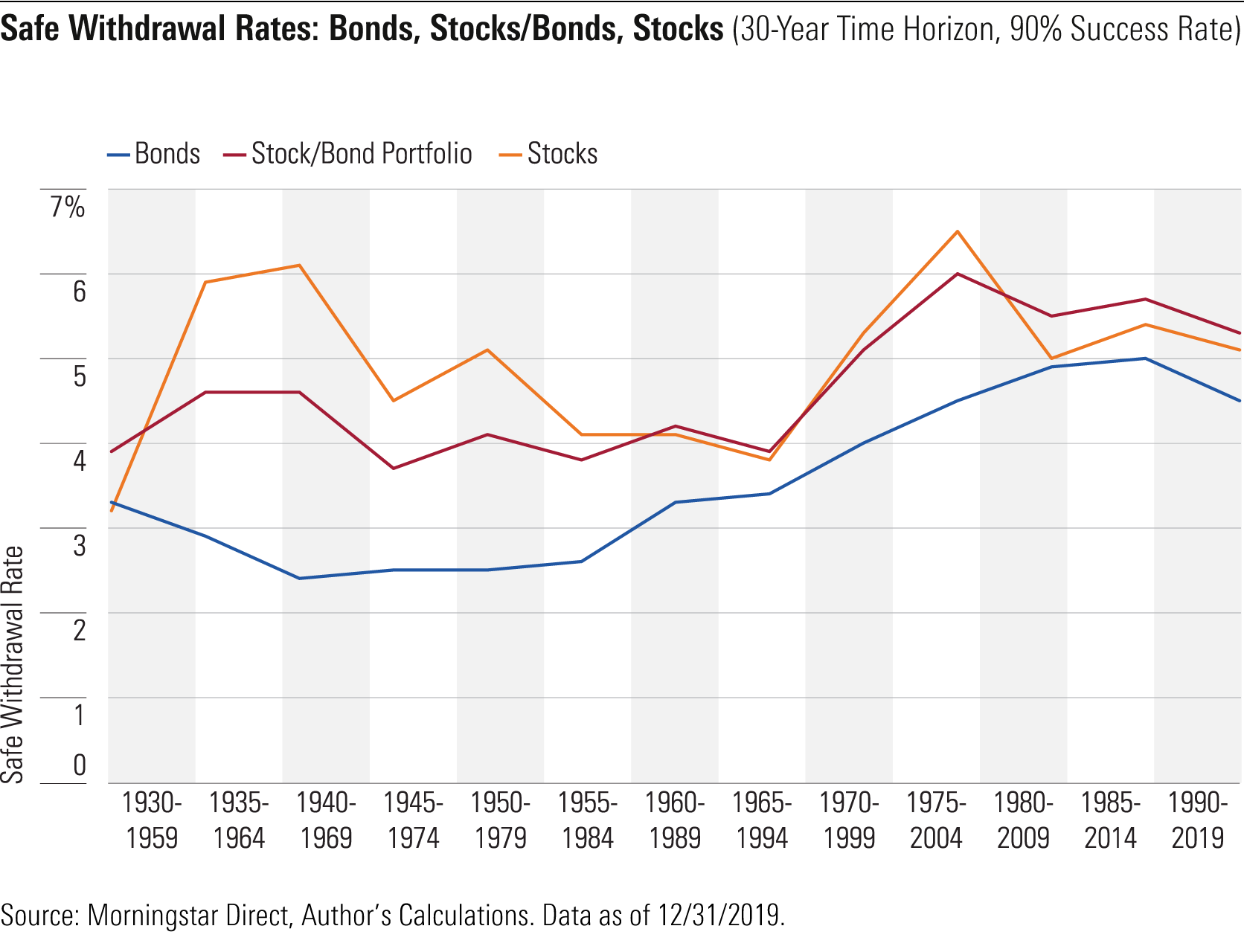

The next chart depicts secure withdrawal fees for U.S. investors around the earlier 80 many years, for a few asset allocations: 1) an intense portfolio consisting of 100% stocks, 2) a reasonable portfolio that retains 50% stocks, 40% bonds, and 10% money and 3) a conservative portfolio that consists of 90% bonds and 10% dollars. The figures are derived by simulating 1,000 likely market performances, applying the normal returns and normal deviations that shares, bonds, and income recorded during people eras, together with the fee of inflation. The protected withdrawal level is defined as the maximum total that can be eliminated for all 30 several years of the simulations without having depleting the portfolio in at the very least 90% of the simulations.

(Be aware: My estimates are somewhat reduced than people computed by Invoice Bengen in his seminal 1994 paper, “Analyzing Withdrawal Fees Utilizing Historical Information.” The discrepancy arises due to the fact Bengen evaluated the single end result of background, whilst I considered additional prospects.)

Supplementing Bonds

Conserve for the preliminary period of time of 1930 as a result of 1959, the seemingly rash tactic of investing of entirely in equities continuously surpassed holding only bonds. Happier still was the middle road. Not at the time did the safe and sound withdrawal price for the bond allocation land in just 50 % a share place of the average portfolio. No matter what the disaster–the Great Melancholy, the stagflation of the ’70s, or the new millennium’s technological know-how-inventory crash–possessing a meaningful stake in shares helped retirees with a 30-calendar year time horizon, instead than hurting them.

Overall, the performances of the intense and moderate portfolios have been about comparable, as measured by harmless withdrawal premiums. The intense allocation led the way via most of the early decades, as equities recovered from their Good Melancholy lows. Success ended up combined more than the future quarter century. Most lately, the inventory/bond blend has moved forward. The vital selection has not been how several equities to keep, but rather to personal them at all.

An additional Watch

Even though cash appreciation is not the main intention for most retirees, help save for individuals who are so rich (or who possess these modest wants) that they will need not be concerned about overspending, it yet is a practical consideration. Far more assets means better money versatility. Retirees can use their added monies to give themselves raises, pay back sudden expenditures, or donate to charities. They might also choose to go away more substantial bequests.

For this secondary intention of capital expansion, equities are paramount. The subsequent chart illustrates the point. It portrays the median final values for the expenditure pools–that is, the median total of assets that keep on being at the conclude of the rolling 30-calendar year periods, right after the essential withdrawals have been funded. For comparison’s sake, every single calculation assumes a $1 million original investment and the same 4.% withdrawal charge. (If the remaining values seem to be pretty significant, that is due to the fact these quantities are calculated in nominal conditions, and consequently include things like 30 years’ well worth of inflation. Even without the influence of inflation, although, the remaining values for the stock portfolios are generally above the beginning amount, when expressed in authentic terms.)

Shares, stocks, and additional stocks! By this evaluate, the competition concerning the intense and average portfolios is no contest. Across all intervals, the 100% fairness allocation steamrolls any system that contains bonds. That even transpired from 1930 though 1959, when the harmless withdrawal charge for the all-fairness portfolio was pretty much a whole percentage level under that of the inventory/bond allocation.

The Whole Distribution

Equities search substantially more powerful because the 2nd chart displays median values, alternatively than the somewhat very poor end result of the 90th percentile that was employed for the withdrawal level chart. Again in the working day, retiree options implicitly assumed median outcomes, but following criticism from Nobel laureate William Sharpe, amid others, habits improved. These days, most retirement-arranging applications goal a significant success fee. My regime was no exception.

Although there’s considerably to be claimed for the new personalized–couple of retirees would willingly concur to plans that were being anticipated to fail 50 % the time!–it does contain a sizeable downside. By basing the investment decision fully on averting negative benefits, the conservative tactic ignores other results. Dodging financial commitment disaster is a great objective. But it must not constitute the whole assessment.

Aside from highlighting a beforehand hidden benefit of the 100% fairness portfolio, the 2nd chart even further demonstrates the hazard of relying entirely on bonds. Not only have fixed-income allocations usually struggled to develop wealth, but for the duration of some 30-yr periods, even their median result has not been enough to fund a 4% withdrawal amount. For retirees looking for to expend an ample sum whilst trying to keep tempo with inflation, bonds have been distinctly unsafe.

Searching Ahead

History’s lesson is clear-cut: the additional shares, the merrier. Investing entirely in equities continuously generated either the optimum secure expending fee for a offered 30-12 months interval, or a rate that wasn’t considerably off the mark. What’s extra, all-fairness portfolios were considerably likelier to deliver a pleased shock than to disappoint.

Need to the upcoming resemble the earlier, the lesson will keep on being legitimate. Retirees should make investments greatly in equities, most likely a lot more than they currently do. But the assistance rests upon that initial assumption. Following Tuesday’s column will appear ahead instead than backward, by checking out how the future time may well be distinctive.

John Rekenthaler ([email protected]) has been exploring the fund sector since 1988. He is now a columnist for Morningstar.com and a member of Morningstar’s expenditure exploration department. John is quick to place out that though Morningstar normally agrees with the sights of the Rekenthaler Report, his views are his have.

More Stories

Market Trends In Organic And Grass-Fed Livestock Products

Challenges And Opportunities In Livestock Export Markets

Insider Inventory Buying Of Canadian Gold Delivers Return On CA$3.00m Investment decision